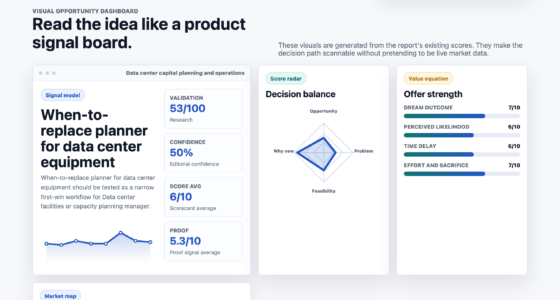

📊 Full opportunity report: The CFO’s new operating system. Anthropic, OpenAI, and the consulting margin that just got compressed. on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

Anthropic and OpenAI are transitioning from model sales to deploying vertical-specific AI operating systems for enterprise finance. This shift, backed by PE investments and new agent templates, is redefining how CFO functions are managed, reducing reliance on traditional consulting and software licensing.

Anthropic has announced a $1.5 billion joint venture with major financial firms to embed its Claude AI into enterprise CFO workflows, signaling a strategic shift from model sales to integrated operating systems. Simultaneously, OpenAI is pursuing a parallel funding round and partnership strategy, reflecting a broader industry move towards vertical integration in enterprise AI.

Between November 2024 and May 2026, the AI enterprise model shifted from selling models to CFOs to deploying pre-built, vertical-specific agent templates integrated into Microsoft 365. Anthropic’s joint venture with Blackstone, Goldman Sachs, and others aims to embed Claude directly into portfolio companies, with ten ready-to-run financial agents launched on May 5, 2026. These agents cover functions like KYC, reconciliation, and earnings review, and are paired with Office add-ins for seamless workflow integration.

Anthropic’s share of enterprise AI spending has risen to approximately 40%, overtaking OpenAI’s 27%, with Ramp data showing Anthropic leading paid adoption at 34.4%, compared to OpenAI’s 32.3%. This indicates a structural shift where the deployment architecture—integrating AI into workflows—is replacing traditional licensing and consulting models, which historically took 18-36 months and 5-10x the software cost.

The new model involves AI labs handling implementation, backed by private equity funding, with the CFO function reorganizing around managed agents deployed rapidly, often within weeks. The consulting layer is responding through partnerships like PwC’s Office of the CFO built on Claude, or through direct disruption via joint ventures, marking a significant industry transformation.

The CFO’s new

operating system.

Anthropic, OpenAI,

and the consulting

margin that just

got compressed.

+ Goldman + Apollo + others JV

Finance Agent benchmark

+ MS365 add-ins shipped May 5

structurally exposed to compression

The AI labs stopped selling models. They are selling operating systems for the Office of the CFO — and the layer that historically sat between the software vendor and the enterprise, the consulting tier, is what gets vertically captured.Thorsten Meyer · The CFO’s New Operating System · Enterprise Reorg 01

Implications of Vertical AI Integration for Enterprise Finance

This shift fundamentally alters the economics and structure of enterprise AI adoption. By integrating model deployment, workflow, and implementation into a single vendor relationship, the traditional consulting and licensing margins are compressed. The move reduces deployment time from years to weeks, lowers costs, and shifts power towards AI labs and private equity-backed deployment models. For CFOs and enterprise decision-makers, this means faster, more integrated AI solutions that could reshape financial operations and valuation dynamics.

AI Workflow Automation for Finance & Administrative Managers: A Practical Guide to Working Smarter in the Age of Intelligent Systems

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Industry Evolution Toward Integrated AI Operating Systems

Over the past 18 months, the enterprise AI market has transitioned from a model of selling standalone AI models to a vertical integration approach, where AI labs deliver pre-built agent templates embedded within workflow platforms like Microsoft 365. Major players like Anthropic and OpenAI are pursuing this shift, backed by substantial private equity investments and strategic partnerships. Anthropic’s $1.5 billion JV and OpenAI’s $4 billion fundraise exemplify this trend, which aims to embed AI directly into enterprise operations rather than selling licenses or consulting services.

This evolution reflects a broader industry pattern: the traditional 1:6 software-to-services revenue ratio is collapsing into a single, more efficient vendor relationship. The deployment architecture now emphasizes rapid, private equity-backed forward deployment, with AI agents serving as the entry point for enterprise finance functions.

“Anthropic and OpenAI have stopped selling models. They are now selling operating systems for the Office of the CFO, packaged as vertical-specific agent templates and deployed rapidly through private equity-backed engineering teams.”

— Thorsten Meyer

Claude AI Made Easy for Accountants: Master Financial Reporting, Tax Preparation, Audit Documentation, Budget Analysis, and Daily Workflow Automation (Claude AI Guide for Beginners Book 13)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Unclear Aspects of Long-Term Adoption and Impact

While deployment architectures and initial adoption metrics are clear, it remains uncertain how widespread and durable this structural shift will be across the entire enterprise industry. Questions remain about the long-term profitability of integrated AI operating systems, potential resistance from traditional consulting firms, and how regulatory or security concerns might influence deployment at scale.

Microsoft 365 Personal | 12-Month Subscription | 1 Person | Premium Office Apps: Word, Excel, PowerPoint and more | 1TB Cloud Storage | Windows Laptop or MacBook Instant Download | Activation Required

- Device Compatibility: Works on Windows and Mac devices

- Included Apps: Word, Excel, PowerPoint, Outlook

- Cloud Storage: 1TB secure cloud storage

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Next Steps in Enterprise AI Deployment and Industry Adoption

Expect further announcements of large-scale joint ventures, additional agent templates, and deeper integration with enterprise workflows. Monitoring the adoption rates among Fortune 500 firms and the responses from traditional consulting firms will be critical. Additionally, the evolution of valuation models for AI-driven enterprise solutions will shape investment and strategic decisions in the coming months.

Securing AI Agents: Foundations, Frameworks, and Real-World Deployment (Advances in Data Analytics, AI, and Smart Systems)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Key Questions

How does this shift affect traditional consulting firms?

Traditional consulting firms may face reduced margins as AI labs and private equity-backed deployment models take over implementation, leading to faster, more integrated solutions that bypass lengthy consulting engagements.

What are the key benefits of these new AI operating systems for CFOs?

They enable rapid deployment of tailored financial agents, reduce operational costs, and streamline workflows within familiar platforms like Microsoft 365, leading to faster decision-making and operational agility.

Will this trend continue across all enterprise functions?

While currently focused on finance, similar architectures are likely to extend to other enterprise functions such as HR, legal, and compliance, as the model proves effective.

What risks are associated with this industry shift?

Potential risks include security vulnerabilities, regulatory challenges, and resistance from established consulting firms, which could slow or complicate widespread adoption.

Source: ThorstenMeyerAI.com